Thinking about saving or investing through an ISA?

But not sure if you’re doing it right?

You are not alone. While ISAs are simple in theory, many people make mistakes that cost them money or stop them from getting the full benefit. Some people pick the wrong type of ISA. Others fail to make the most of their annual allowance. And many leave their cash sitting idle when it could be working harder.

In this guide, we’ll cover five of the most common ISA mistakes and, more importantly, how you can avoid them. By the end, you’ll have a clear action plan backed by practical financial advice to build a stronger financial future with confidence.

What is an ISA? A Quick Refresher

Before we dive into the ISA mistakes, let’s take a moment to recap what an ISA actually is. An ISA is a tax wrapper for your savings or investments. The government sets a limit each year on how much you can put into ISAs.

For the 2024/25 tax year, that allowance is £20,000.

The big benefit is that any money you put in an ISA grows tax-free. That means you don’t pay income tax on interest from a Cash ISA, and you don’t pay capital gains tax or dividend tax on investments held in a Stocks and Shares ISA.

There are several types of ISAs:

- Cash ISAs

These work like a savings account but with tax-free interest.

- Stocks and Shares ISAs

Your money is invested in funds, shares, or bonds. Returns are tax-free.

- Lifetime ISAs (LISAs)

Designed for first-time buyers or retirement savings, with a government bonus.

- Junior ISAs (JISAs)

Savings accounts for children, with tax-free growth.

Now that we’ve covered the basics, let’s look at the common pitfalls.

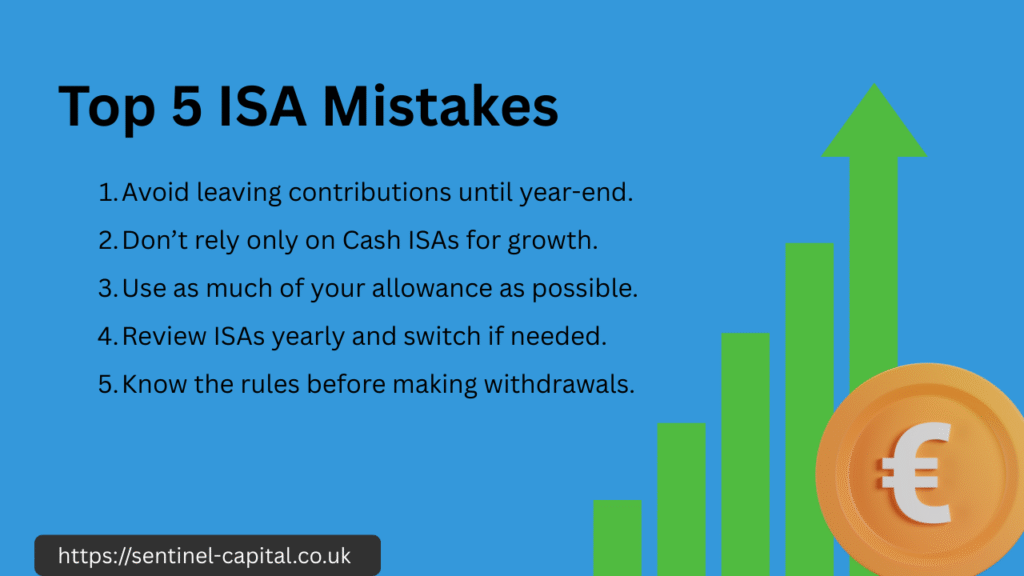

ISA Mistake 1: Leaving Your ISA Contributions Until the End of the Tax Year

One of the biggest mistakes people make is waiting until the end of the tax year to put money into their ISA. Technically, you have until the 5th of April to use your allowance, and many people wait until March to make a lump-sum contribution.

Most people put off contributing because they think they need a big lump sum, but even small amounts can build up through the power of compound growth. Some underestimate the impact of compound growth.

Others delay because they’re unsure where to invest. However, procrastination or poor planning eventually leads to missed opportunities.

By waiting, you miss out on the opportunity for your money to grow during the year. Whether you’re earning investment returns in a Stocks and Shares ISA or getting a 25% bonus for LISA on your contributions, the earlier you put money in, the longer it has to compound.

Example

Imagine you put £10,000 into your ISA on April 6th at the start of the tax year. If your investments grow by 5 percent, by the following April you’ll have £10,500.

But if you wait until March to invest that £10,000, you’ll only have one month of growth, which could be just £40 or £50. Over decades, those lost months of growth can add up to thousands.

How to Avoid It?

- Try to spread contributions throughout the year, either with a lump sum at the start or through monthly deposits.

- If you have spare cash sitting in a current account, consider moving it into your ISA sooner rather than later.

- Even small monthly contributions can make a big difference thanks to compound growth.

ISA Mistake 2: Sticking Only to One Type of ISAs

Many savers make the mistake of depending on just one ISA option, such as a Stocks and Shares ISA or a Lifetime ISA, without considering whether it truly matches their goals. While both can be powerful tools, using them in isolation may limit your overall financial growth.

Why It’s a Problem?

- A Stocks and Shares ISA offers long-term growth potential, but your investments are exposed to market ups and downs. If you need money in the short term, this risk could work against you.

- A Lifetime ISA is great for first-time home buyers or retirement savings, but it comes with strict withdrawal rules and penalties if you need the money for anything else.

- Focusing only on one ISA may leave you without the flexibility or balance you need in your finance strategy.

How to Avoid it?

Instead of relying solely on one type of ISA:

- Mix ISA types to balance flexibility and growth potential.

- Pair a Stocks and Shares ISA with a Lifetime ISA if you want both investment growth and government-backed bonuses.

- Seek professional financial advice to make sure your ISA choices align with your personal timeline and goals.

By diversifying how you use ISAs, you avoid unnecessary limits and make your savings work harder for your future.

ISA Mistake 3: Not Making the Most of Your ISA Allowance

Each tax year, you’re given a fresh ISA allowance (£20,000 for 2024/25).

The catch is that it’s strictly a “use it or lose it” benefit. If you don’t contribute the full amount before the 5th of April, any unused allowance disappears and can’t be carried over into the next year.

Many people assume that contributing a small portion of their allowance is good enough. While it’s always better to save something than nothing, not maximising your allowance means missing out on years of tax-free growth.

Example:

If you invest the full £20,000 each year in a Stocks and Shares ISA for 20 years with an average 5% return, you could end up with more than £650,000. But if you only put in half (say £10,000 annually), you’d have roughly half that amount. Over decades, the difference is life-changing.

The allowance is designed to give you as much tax-free growth as possible, so leaving it underused is like turning away free benefits.

How to Avoid it?

- Set up regular contributions (monthly or quarterly) to make steady use of your allowance instead of rushing at the year-end.

- Top up with extras like work bonuses, tax refunds, or unexpected income rather than letting them sit idle in a current account.

- Split your allowance smartly between ISA types. For example, combining a Stocks and Shares ISA for long-term growth with a Lifetime ISA if you’re saving for a first home or retirement.

- If you’re unsure how much to allocate or which ISA mix is right for your timeline, seek expert financial advice to structure your contributions most effectively.

Making full use of your ISA allowance every year can significantly shape your long-term wealth and give you a powerful head start on financial freedom.

ISA Mistake 4: Forgetting to Review or Switch ISAs

Another common mistake is treating your ISA as a “set it and forget it” account. While it’s true that ISAs are long-term savings vehicles, it doesn’t mean you should ignore them completely.

The right mix of investments or savings options can shift depending on whether you’re just starting out, building wealth, or preparing for retirement. Besides that, your goals today may not be the same in five or ten years. Reviewing your ISA helps keep your savings in line with where you’re heading.

A quick review shows you how your ISA is performing and whether it’s on track for the milestones you care about. Knowing your ISA still suits your situation helps you feel more secure about the future.

How to Avoid it?

- Check your ISA once a year to see if it still reflects your financial goals.

- Shift Your Investment Strategy as Priorities Change. For example, you might want to move from growth-focused investments to income-focused ones as you get closer to retirement.

- Consider your choices between Stocks and Shares ISAs or Lifetime ISAs, depending on what you’re working toward. If you find a better deal, use the official ISA transfer process. Don’t withdraw the money yourself, or you’ll lose the tax benefits.

- Get professional input if needed, especially if you’re unsure whether to make changes.

Taking a little time to review your ISA means you’ll always know your money is working in a way that feels right for you.

ISA Mistake 5: Withdrawing Money Without Thinking About the Rules

One big advantage of ISAs is easy access to your money. But there’s a catch. Not all ISAs are flexible. With a standard ISA, if you take money out, it still counts towards your allowance.

For example, if you put £20,000 into an ISA and then withdraw £5,000, you can’t put that £5,000 back in the same year. You’ve used your full allowance.

This is where understanding ISA types matters. Some ISAs are flexible, meaning you can withdraw and replace funds within the same tax year without losing allowance space. Not every ISA offers this, so it’s important to know how yours works.

How to Avoid It?

- Always check whether your ISA is flexible before making a withdrawal.

- Match the ISA type to your goal. For example, Lifetime ISAs are better for long-term plans like retirement or a first home.

- Try to leave your ISA untouched when possible. The longer your money stays invested, the greater its potential to grow.

Other ISA Mistakes to Watch Out For

Beyond the five main ISA mistakes, there are a few extra areas where investors sometimes slip up:

- Forgetting old ISAs

Over the years, it’s easy to lose track of older accounts. Scattered savings can be less effective, and some may sit in underperforming funds. Reviewing and consolidating can help keep your money working harder.

- Overlooking a Lifetime ISA

If you’re under 40 and planning for your first home or retirement, a Lifetime ISA could be a valuable option. The 25% government bonus on contributions is money many people miss out on simply by not exploring it.

- Investing without understanding risk

Stocks and Shares ISAs can offer stronger growth potential than cash, but they also carry risk. The key is to choose an approach that fits your goals and comfort level.

FAQs

Can I have more than one ISA?

Yes. You can hold more than one ISA at the same time, but you can only pay into one of each type per tax year. For example, you could contribute to a Stocks and Shares ISA and a Lifetime ISA in the same year, but not two Stocks and Shares ISAs with different providers.

Can I lose money in a Stocks and Shares ISA?

It’s possible. Since your money is invested in the stock market, its value can go up and down. While the long-term trend has historically been positive, short-term dips are normal. That’s why it’s important to choose investments that match your goals and risk comfort.

What happens to my ISA when I die?

Your ISA becomes part of your estate, but some rules allow your spouse or civil partner to inherit the tax benefits through an “additional permitted subscription.” This means they can continue to benefit from your ISA savings.

Can I open a new ISA every year?

Yes. Each tax year, you get a fresh ISA allowance. You can open a new ISA with the provider of your choice or keep contributing to an existing one, as long as you stick within the allowance limits.

Can I transfer my ISA to another provider?

Yes. You can transfer your ISA at any time without losing your tax benefits, but you must use the official transfer process. Never withdraw the money yourself, as you’ll lose the ISA wrapper and tax advantages.

What’s the difference between a flexible and a non-flexible ISA?

With a flexible ISA, you can withdraw money and put it back in within the same tax year without affecting your allowance. Non-flexible ISAs don’t allow this, meaning once you withdraw, that portion of your allowance is gone.

How much does the government add to a Lifetime ISA?

If you’re eligible for a Lifetime ISA, the government adds a 25% bonus to your contributions, up to a maximum of £1,000 per year. This can make a big difference if you’re saving for your first home or retirement.

Final Thoughts: Make the Most of Your ISA

With the right approach, your ISA can be a reliable tool to help you reach your financial goals. Avoiding common mistakes really makes the most of your ISA. It gives you tax-free growth, flexibility, and options that fit different goals.

Don’t wait until the end of the year to add money. Use as much of your yearly allowance as you can, and know the rules before taking money out.

Whether you’re putting money aside for a first home, your children, or retirement, starting early and staying consistent will put you in a stronger position for the future.

If you want your ISA to do more than just sit in an account, it helps to know the rules and choose the right type of plan for your goals. With Sentinel, you get clear options and support to make smarter choices for your future.

Contact now for expert ISA consultation.